This Vermont health insurance guide, including the FAQs below, will help you understand the coverage options and potential financial assistance available to you and your family.

Vermont runs its own health insurance exchange (Marketplace), which is called Vermont Health Connect . The Vermont Health Connect platform allows residents to shop for individual and family health plans offered by two private health insurance carriers. These plans are used by people who aren’t eligible for Medicare, Medicaid, or an affordable employer-sponsored health plan. Vermont Health Connect can also be used to enroll in Medicaid or Dr. Dynasaur .

Vermont is among the states that offer state-funded subsidies in addition to the federal subsidies provided under the ACA. Vermont is also among the states that have individual mandates , but unlike the other states that have individual mandates, Vermont does not have a financial penalty for going without coverage. 1

As explained in more detail below, premium subsidies in Vermont are expected to be “much larger” in 2025 than they were in 2024, 2 due to the state’s new approach for setting Silver plan rates. For most enrollees, this will more than offset the overall weighted average rate increase of 18.1% that has been approved for Vermont’s individual market plans.

Vermont’s individual and small group health insurance markets were merged (unlike most other states) through 2021, but were separated as of January 2022. 3 Without additional legislation, they will re-merge starting in 2026. 4

Hoping to improve your smile? Dental insurance may be a smart addition to your health coverage. Our guide explores dental coverage options in Vermont.

Learn about Vermont's Medicaid expansion, the state’s Medicaid enrollment and Medicaid eligibility.

Use our guide to learn about Medicare, Medicare Advantage, and Medigap coverage available in Vermont as well as the state’s Medicare supplement (Medigap) regulations.

Short-term health plans provide temporary health insurance for consumers who may find themselves without comprehensive coverage. Learn more about short-term plan availability in Vermont.

To be eligible to enroll in private health coverage through Vermont Health Connect, you must:

So most people in Vermont are eligible to enroll in a health plan through Vermont Health Connect. But there are some additional parameters must be met in order to qualify for state and federal subsidies through Vermont Health Connect.

To qualify for income-based federal Advance Premium Tax Credits (APTC), federal cost-sharing reductions (CSR), or Vermont’s state-funded financial assistance you must:

In addition to those basic parameters, Vermont Health Connect premium subsidy eligibility will depend on your household’s income and how it compares with the premium for the second-lowest-cost Silver plan in your area (unlike most states, premiums do not vary by age or location within the state of Vermont).

The open enrollment period in Vermont begins November 1 and continues through January 15. 8

Enrollments must be completed by December 15 to have coverage effective January 1. Enrollments completed between December 16 and January 15 will have a February 1 effective date. 9

Outside of the annual open enrollment period, you may still be able to enroll or make a plan change if you experience a qualifying life event, such as giving birth or losing other health coverage.

Some people can enroll year-round even without a specific qualifying life event . This includes the low-income special enrollment period, which is available to Vermont applicants with household income up to 200% of the poverty level. 10 (The household income cutoff for this SEP is 150% in most states.)

Enrollment in Vermont Medicaid and Dr. Dynasaur is available year-round for eligible applicants.

To enroll in an ACA Marketplace/exchange plan in Vermont, you can:

You may find that you’re eligible for financial assistance through Vermont Health Connect, which can make your coverage and medical care more affordable. And the assistance may be more robust than it is in many other states, as both federal and state subsidy programs are available in Vermont .

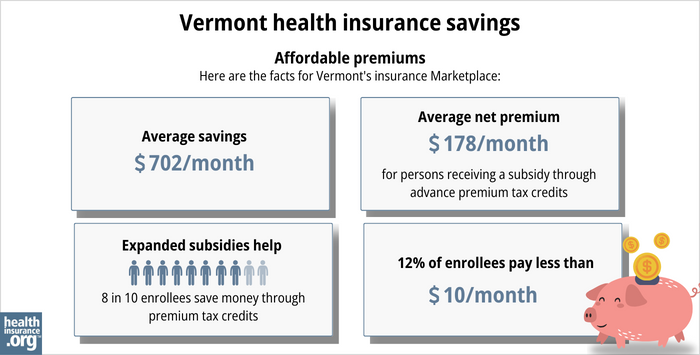

The Affordable Care Act (ACA) created federal premium subsidies (advance premium tax credits, or APTC), which are available depending on your income. Nearly nine out of ten Vermont Health Connect enrollees (89%) were receiving APTC as of early 2024. These subsidies covered an average of $702/month, reducing the average enrollee’s premium to about $243/month. 12

Vermont also offers state-funded premium subsidies for applicants with household income up to 300% of the federal poverty level. The additional subsidies stack on top of the federal APTC, and reduce (by 1.5 percentage points) the percentage of income that applicants have to pay to purchase the second-lowest-cost Silver plan. 13

Federal cost-sharing reductions (CSR) are available to applicants with household income up to 250% of the poverty level, and Vermont offers additional cost-sharing reductions to bring eligibility for this program up to 300% of the poverty level in Vermont. 14

Cost-sharing reductions reduce the deductible and other out-of-pocket expenses for Silver-level plans. Nearly 28% of Vermont Health Connect enrollees were receiving CSR benefits as of 2024. 15

Depending on your income and circumstances, you may be able to enroll in free or low cost health coverage through Vermont Medicaid or Dr. Dynasaur. Learn more about whether you might be eligible for these programs in Vermont.

Two insurance companies offer health plans through Vermont Health Connect, and both will continue to offer coverage in 2025. 17

Approved 2025 rate changes for Vermont’s insurers are shown below, but it’s important to note that Vermont’s premium subsidies are expected to be significantly larger in 2025 due to a new state requirement for how Silver plan premiums are set. According to the Green Mountain Care Board, “despite significant increases in the gross premiums of individual plans, for most people, the net premiums, after accounting for premium subsidies, are expected to decrease.” 2

Starting with the 2025 plan year, Vermont is joining Texas and New Mexico in requiring carriers to add a specific and significant load to Silver plan rates to account for the fact that the federal government no longer funds cost-sharing reductions (that has been the case since 2018, but carriers have set their own CSR loads until now). 18

Specifically, the carriers have to add a 41.9% load to Silver plan rates to account for the cost of CSR (for reference, New Mexico requires a 44% load and Texas requires a 35% load; Pennsylvania also has a state-mandated protocol for this, but the load is only 22%-26%, 19 so it’s not as significant).

This will result in Vermont Health Connect’s Gold plans being priced lower than Silver plans. It will increase premium subsidies for everyone who qualifies for them, and make non-Silver plans tend to be the more attractive option for people who aren’t eligible for cost-sharing reductions. 20

The following table shows Vermont’s Marketplace insurers’ approved rate changes for 2025 individual/family health plans, 2 amounting to a weighted average rate increase of 18.1% before any subsidies are applied. 21

As noted above, however, subsidies will be larger in 2025 for subsidy-eligible enrollees, resulting in lower net premiums for many enrollees.

Source: Green Mountain Care Board 17

The approved rates are larger than the carriers initially proposed, but smaller than the revised proposals the carriers submitted. Green Mountain Care Board noted that they “had limited latitude this year to require further reductions to the proposed premiums” due to concerns about a carrier’s financial viability. 2

Ninety-one percent of Vermont Health Connect enrollees receive premium subsidies, 22 which will grow disproportionately to overall premiums in 2025, making net premium lower for many enrollees. But for the 9% of enrollees who don’t get subsidies, plus anyone enrolled outside the exchange (as well as businesses with small group health plans), the regulators note that the approved rates for 2025 are “painfully high.” 17

For perspective, here’s a summary of how average pre-subsidy rates have changed in previous years in Vermont’s individual/family market:

*For both insurers, the approved rates for 2018 were based on the assumption that federal funding for cost-sharing reductions (CSR) would continue. But on October 12, 2018 (less than three weeks before the start of open enrollment) the Trump administration announced that funding for cost-sharing reductions (CSR) would end immediately. Insurers in many states had already prepared for this eventuality in their rate filings, although some states scrambled in the subsequent days to revise rate filings to add the cost of CSR to 2018 premiums. Vermont, however, stuck with the rates that had been approved in August — which were based on the assumption that the federal government would continue to fund CSR.

But even if Vermont’s insurers had been allowed to add the cost of CSR to premiums for 2018, the impact would have been smaller than it was in most states. This is due in large part to the fact that the individual and small group risk pools were combined in the state (until 2022), meaning that an increased cost situation that impacted rates for the individual market was spread across the small group market too, resulting in a more stable rate situation.

In 2019, Vermont’s insurers were allowed to start adding the cost of CSR to silver plan premiums under the terms of S.19, as is the protocol used in most states. As explained above, the state has begun requiring carriers to add a 41.9% CSR load to silver plan rates starting with the 2025 plan year.

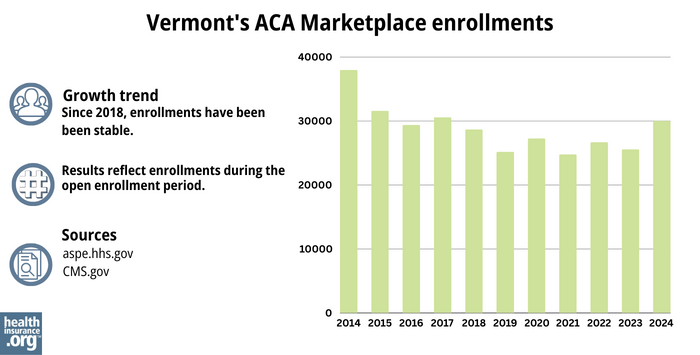

During the open enrollment period for 2024 coverage, 30,027 people selected private plans through Vermont Health Connect. 15 This was the highest enrollment had been since 2017.

Source: 2014, 33 2015, 34 2016, 35 2017, 36 2018, 37 2019, 38 2020, 39 2021, 40 2022, 41 2023, 42 2024 43

Vermont Health Connect

The state-run health insurance Marketplace/exchange. Individuals and families use the Marketplace to obtain health coverage, with financial assistance based on income. Vermont Health Connect can also be used to enroll in Medicaid and Dr. Dynasaur.

Vermont Insurance Division

Consumer assistance with insurance questions and complaints.

Green Mountain Care Board

An independent five-member board, created by Vermont’s 2011 health care reform legislation and tasked with improving health care transparency, advancing innovation in health care payment and delivery, and regulating various aspects of health care in the state. The Green Mountain Care Board is also responsible for reviewing and approving health insurance rates.

Vermont State Health Insurance Program

A local service that provides enrollment counseling and assistance for Medicare beneficiaries.

Vermont Medicaid and Dr. Dynasaur

Health coverage for low-income Vermont residents.

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written dozens of opinions and educational pieces about the Affordable Care Act for healthinsurance.org.